A report commissioned by the FRDC has found there is no single seafood industry COVID-19 story, but a range of experiences from positive to catastrophic and everything in between

By Annabel Boyer

caption caption Photo: credit

In 2020, at the height of the COVID-19 pandemic, the FRDC commissioned a report to better understand the pandemic's impact on Australia's seafood industry and the industry's response as the two unfolded together.

The rationale behind the report was that no crisis should be wasted; it could provide fertile ground for insights to deal with other, future challenges. It aimed to gain a broad understanding of the immediate economic impacts to the industry from the early phases of the COVID-19 pandemic.

The team at the University of Tasmania's Institute for Marine and Antarctic Studies (IMAS) put together the report, led by social scientist Emily Ogier.

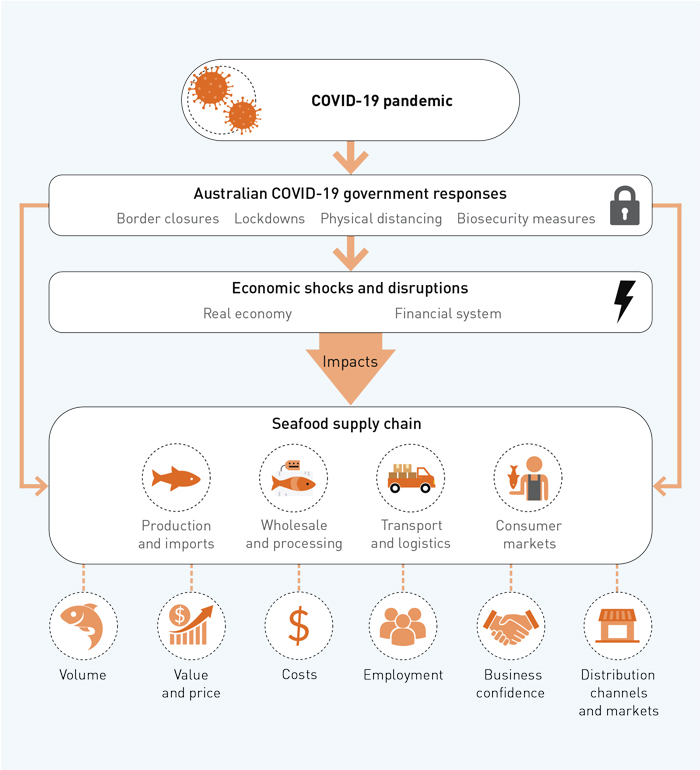

It focuses on the short-term impacts of the early stage (January–June 2020) of the COVID-19 pandemic on the Australian seafood industry and examines the impacts at a sector level, rather than at an individual business level.

"We assembled quantitative and qualitative evidence from multiple sources including government and management datasets, industry survey data, published market research and stakeholder interviews," says Emily Ogier. "The combination of all this data builds a picture of how the industry, across the entire supply chain, faired during the period.

"The value of Australia's seafood product and its people, and the impacts they experienced, are really challenging to capture through the data that is available. We threaded narratives together from mixed sources.

"We asked: what is the market showing? Is this reflected in what industry leaders and producers are saying? How did that transmit to actual production? What is a sensible baseline to understand before, during and after COVID-19 lockdowns? What level of change is normal variation and what is impact? How can we measure the uncertainty and personal costs to producers and business sustainability?"

Not all of the impacts recorded can be definitively linked to COVID-19. Nevertheless, the report provides valuable clues as to the vulnerabilities of Australia's seafood industry and what needs to change to make businesses and supply chains more resilient.

Broad impacts

Broadly, the report found impacts have been asymmetric: economically significant sectors that relied on one or two export markets have been badly affected, while other sectors supplying domestic markets have generally prospered. Businesses, irrespective of sector, that have been both willing and able to be innovative and agile have also benefited.

The businesses most negatively impacted were live export and dine-in food service, due to their reliance either on international air freight or on people moving about in their communities, both of which were restricted. Businesses most positively impacted were those serving domestic retail and takeaway food service markets, which experienced a rise in demand and, in some cases, prices, too.

During the period examined, export products declined in both value and volume. In contrast, the value of domestic products remained relatively stable and a decline in volume was offset by a rise in prices.

As the crisis progressed, domestic production, which initially fell, rebounded as producers adapted. The report highlights a number of innovative responses to the challenge at hand. Businesses were also crucially helped along by the easing of restrictions halfway through the period examined.

Government support measures provided valuable support to allow for profitability and business continuity during the period of disruption.

In general, the report found COVID-19 has exacerbated the uncertainty caused by other challenges such as drought, bushfires and exchange rate fluctuation being faced by Australia's seafood businesses.

"We assembled quantitative and qualitative evidence from multiple sources including government and management datasets, industry survey data, published market research and stakeholder interviews." Emily Ogier, University of Tasmania

An ongoing learning experience

While the report is a snapshot of a particular time period, the COVID-19 disruption continues and further indirect effects are being experienced.

The seafood industry's recovery and the development of greater resilience is still evolving. Differences in degree of exposure, impact and recovery will continue across sectors of the Australian industry.

Three stages of assessment

The report assesses impacts on the various parts of the industry and along the supply chain from producer to retailer.

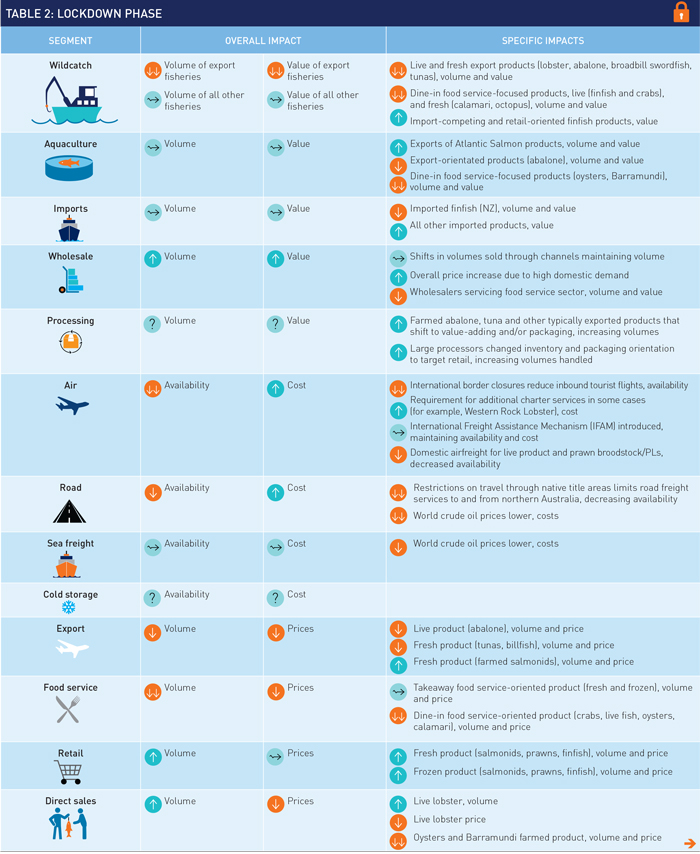

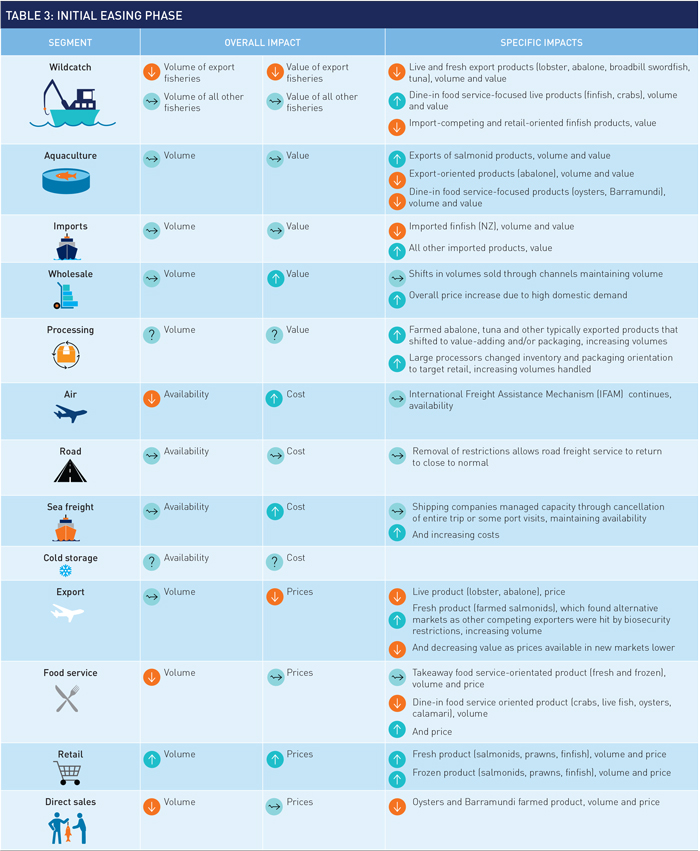

It divides the time period examined into three distinct phases: the shock phase (January–March), the lockdown phase (March–May) and the initial easing phase (May–July).

The shock phase (Table 1) is characterised by the initial outbreak in China, the lockdown in Wuhan and the restriction of Chinese New Year celebrations, which impacted certain limited sections of the Australian seafood industry such as the export sector.

The lockdown phase (Table 2) starts with the emergence of an Australian outbreak of the virus, the closure of national and state borders, the announcement of lockdowns and physical restrictions.

The initial easing phase (Table 3) starts with the easing of lockdown measures in some states, the return of exports to normal levels, the emergence of secondary outbreaks and the planned reopening of some borders.

To read the full report, including in-depth analyses of the impact on different parts of the seafood production and supply chain, and case studies showcasing industry responses to the crisis, go to the FRDC project 2016-128.

The report findings were presented at the Outlook 2021 Conference, which was held from 2–5 March. The full program is available at ABARES.

More information

Emily Ogier, emily.ogier@utas.edu.au

FRDC RESEARCH CODE: 2016-128